By Fergus Nelson and Madeline Combe

Find this Article on Altiorem

In 2015, the creation of the Task Force on Climate-Related Financial Disclosures (TCFD) facilitated a standardised climate-related risk disclosure framework. Some of its end users include banks, insurance companies, asset managers, asset owners and other non-financial corporate participants from industries such as energy, transportation, construction and agriculture. Its aim is to increase the transparency of a given company’s exposure to climate-related risks and opportunities, in order to ensure the stability of the financial system and promote the transition to a more sustainable economy. As of July 2022, there are more than 3,400 companies from 92 countries with a combined market capitalisation of US$27.2 trillion that have committed to support the TCFD recommendations.

Following a similar logic, the Task Force on Nature-Related Financial Disclosures (TNFD) was launched in June 2021, with the second beta version released in June 2022. Its goal is to provide a framework for organisations to report and act on evolving nature-related risks and opportunities, thus supporting a shift in global financial flows away from nature-negative outcomes and toward nature-positive outcomes. Just as the TCFD (and its immense popularity) signalled the consensus that climate change presents a material risk to global markets — one demanding disclosure — the launch of the TNFD highlights further maturation in our relationship to risks borne from the natural world. The TNFD builds upon the same approach taken to the development of the TCFD and aligns with existing initiatives such as the Global Reporting Initiative (GRI), Sustainable Accounting Standards Board (SASB), Climate Disclosure Standards Board (CDSB), and International Financial Reporting Standards (IFRS), as well as the global baseline for sustainability standards which is currently being developed by the International Sustainability Standards Board (ISSB). Past practices for reporting on nature have been consolidated to create a standardised industry framework.

The development of the TNFD has been made possible by the 34 senior executives which make up the TNFD Taskforce. The Taskforce collectively represents businesses with over US$19.4 trillion in assets under management across over 180 countries. Elizabeth Maruma Mrema, the Executive Secretary of the United Nations Convention on Biological Diversity, stated in her opening remarks at COP15 in 2022, that:

“The business and financial sectors have a central role to play in shifting global financial flows from negative to positive outcomes for nature. Identifying and disclosing their dependencies and impacts on nature, and the associated risks, is an essential step in this transition. The Taskforce on Nature-related Financial Disclosures (TNFD), which I have the honour to co-chair, will help them to achieve this”.

As part of COP15’s Kunming Declaration, 99 ministers, 9 heads of state and the heads of delegations have committed to adopt and implement an effective post-2020 Global Biodiversity Framework. The TNFD will play an instrumental role in this commitment.

The TNFD are guided by the following seven principles:

- Market Usability: Develop frameworks that are useful and valuable to market reporters, users and policy makers

- Science Based: Follow a scientifically anchored approach, incorporate well established and emerging scientific evidence

- Nature-related risks: Embrace nature-related risks that include immediate, material financial risks as well as dependencies and impacts on nature dependencies

- Purpose-driven: Actively target reducing risks and increasing nature-positive actions

- Integrated and Adaptive: Align with existing frameworks and adapt to future developments

- Climate-Nature Nexus: employ an integrated approach & scale finance for Nature-Based Solutions

- Globally Inclusive: Ensure the framework is relevant, just, valuable, accessible and affordable worldwide

Why do we need it?

The need for TNFD comes due to the impending impacts of climate change on nature and ecosystems. It is estimated that due to human activity, almost 1 million species are at risk of extinction according to the 2019 Global Assessment Report of the Intergovernmental Panel of Biodiversity and Ecosystem Services (IPBES). The World Economic Forum’s 2020 Global Risks Report identifies biodiversity and ecosystem collapse as one of the top five threats humanity will face in the next 10 years. Additionally, the threat of ecosystem collapse also presents significant economic ramifications, as over half of global GDP (around US$44 trillion) is reliant on nature and therefore potentially threatened.

The stock of Earth’s natural capital has also been severely depleted. Natural capital encompasses our stock of natural assets, including geology, soil, air, water and all living things. The OECD definition of natural capital splits natural assets into three groups: natural resource stocks, land and ecosystems. It is estimated that the global stock of natural capital has declined by 40% between 1992 and 2014. Natural capital also plays a vital role in providing ecosystem services, which are the direct and indirect benefits that flow from nature to humans as a product of the interactions between natures living and non-living elements. For example, a tree within a forest can filter water, sequester carbon, provider food and shelter to many species and help regulate the climate and nutrient cycles. Shocks to ecosystems such as extreme weather, deforestation, carnivore removal can significantly hinder the ability to provide these beneficial and free ecosystem services.

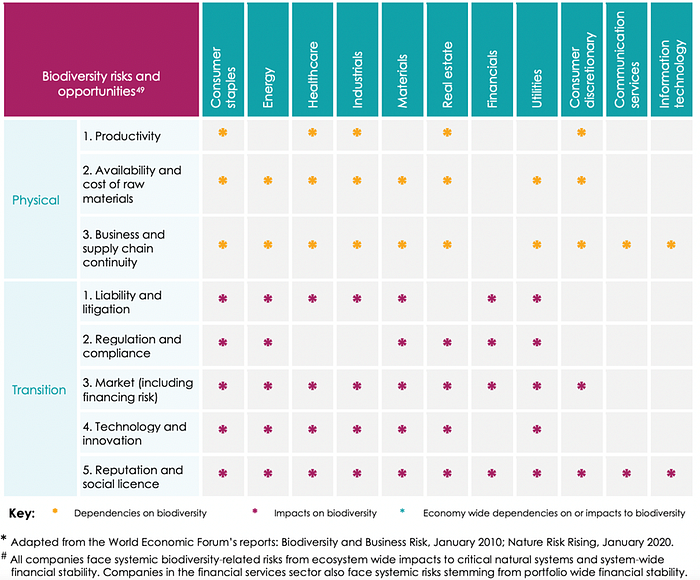

The economic impact of ecosystem service breakdown is noteworthy; the 2019 IPBES report predicts that between US$235–577 billion worth of annual crop value is at risk due to insufficient pollination, which sustains 71 of the most commonly used crops. Bringing our focus to Australia, ACSI’s Biodiversity: Unlocking natural capital value for Australian Investors report predicts that by 2050, the Australian economy could lose up to US$20 billion annually due to nature loss. Our economy’s dependency on biodiversity (mostly through primary industry) means that all industries are exposed to varying levels of risk due to biodiversity loss. Figure 1 breaks down the risks and opportunities faced by different sectors of the economy.

It is proving to be increasingly difficult for even the most diversified portfolios to avoid exposure to risk created by biodiversity loss. The same ASCI report identifies financial material risks created by biodiversity loss, including credit risk, risk to investments and capital, market risk, liquidity and insurance. These risks are becoming more immediate, as a recent report has found that Australia has already transgressed its national limit for the global biosphere integrity boundary, the limit beyond which biodiversity can no longer support ecosystem processes and resilience.

The establishment of a nature reporting framework such as the TNFD is essential for companies to measure their impacts, dependencies, and risk on nature (both positive and negative). While scientific reporting on biodiversity is abundant, the TNFD presents a standardised way for companies to assess and measure their risks associated with nature. This allows businesses to manage and plan their business operations accordingly, creating transparency and security for investors as well.

How does the TNFD define nature?

It’s important to clarify the difference between nature and biodiversity, as the two terms are often used interchangeably. Within the context of the TNFD framework, nature is defined as “the natural world, with an emphasis on the diversity of living organisms (including people) and their interactions among themselves and with their environment”. On the other hand, biodiversity refers to the “variability among living organisms from all sources, including, inter alia, terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are part; this includes diversity within species, between species and of ecosystems”. Put simply, nature refers to the presence of biotic and abiotic elements (including natural processes such as currents and climate regulation) while biodiversity is concerned with the variety of organisms present. For example, a palm oil plantation may be considered natural because palm oil comes from trees, but it has come at the expense of biodiversity through deforestation, the use of pesticides and other human interventions.

Within the TNFD, nature is defined to include both biotic and abiotic (living and non-living) elements. Living nature is inclusive of habitats, species and genetic resources across land, ocean, lakes and rivers. Non-living nature is made up of soil, water and air, for example. These non-living nature components have complex interactions with living nature to produce what are called ecosystem services, such as water filtration and flood protection. Nature also encompasses the Earth’s stock of minerals; their extraction through mining or other methods can create negative effects on ecosystems.

LEAP Framework

One key tool of the TNFD is LEAP (Locate, Evaluate, Assess, Prepare): an integrated nature-related risk and opportunity assessment process. Figure 2 goes into detail for each stage of the LEAP assessment process. The LEAP approach intends to support corporates and financial institutions carry out internal, nature-related risk and opportunity assessments. The findings of a LEAP assessment will then be used to inform strategy, governance, capital allocation and risk management decisions. This includes disclosure decisions adhering to the TNFD’s draft disclosure recommendations.

How to prepare for the TNFD

In order to prepare for the arrival of the TNFD, investors, corporates, financial institutions and asset managers are encouraged to take the following steps. Firstly, they should start identifying short, medium and long-term exposure to nature-related risks in their current portfolios and value chains. Secondly, they should consider utilising appropriate nature-related metrics, targets and internal reporting mechanisms. Thirdly, they should actively engage company boards to determine how exactly nature-related risk will affect normal business operations. Next, they should familiarise themselves with the prototype LEAP approach as well as the extended LEAP-FI for Financial Institutions. Finally, check resource availability and consider pilot testing the TNFD/LEAP framework and submitting a case study.

Timeline

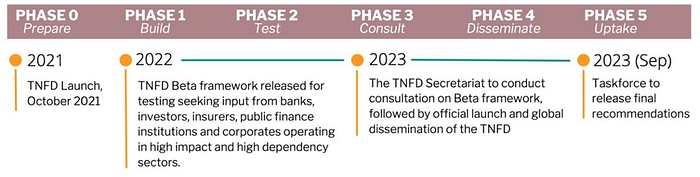

The TNFD will be rolled out in stages, with each stage increasing in complexity to allow organisations to help organisations transition in applying the framework. Figure 3 shows a summary of the key phases and timeline of the TNFD Beta Frameworks.

What the TNFD means for retail investors

The advent of the TNFD is a step in the right direction for mapping the economy’s interactions with nature. Our dependency on nature means there are few industries not exposed to the risks associated with biodiversity loss. The TNFD allows businesses to manage and plan their business operations accordingly, creating transparency and security for investors as well.

While mandatory reporting on the TNFD is still a while off, shareholders can engage companies to voluntarily report their impacts on nature. Shareholders have a right to know how their investments affect and are affected by nature and can make their influence felt through raising the TNFD at Annual General Meetings.

As we start to unravel the complexities of our relationship with Nature, it is clear how inextricably linked humans are with the natural world. The TNFD provides a means by which businesses and investors can map their many connections to nature and identify which of their activities are at most risk of degrading her at the expense of the economy and society. It’s vital that we begin to view the economy as embedded within ecological and social systems. Through the introduction of the TNFD, we can begin to bridge the gap of understanding business risk associated with nature.